Which Crypto Projects Make the Most Money? Most Profitable Blockchains by Revenue (2026)

Apr 23, 2026 03:37

Last updated: April 2026 | Data sources: Token Terminal, DefiLlama, CoinGecko Research

Most people still evaluate crypto by price charts. That is the wrong move. Price follows revenue - not the other way around. After spending years watching projects pump on narrative and then bleed out because there was no real business underneath, I can tell you: the one number worth checking before anything else is protocol revenue.

This article breaks down which crypto projects are actually generating money right now, what their revenue model is, and how to read on-chain revenue data yourself without getting fooled by vanity metrics.

What Does "Revenue" Mean in Crypto?

Before getting into the rankings, this distinction matters.

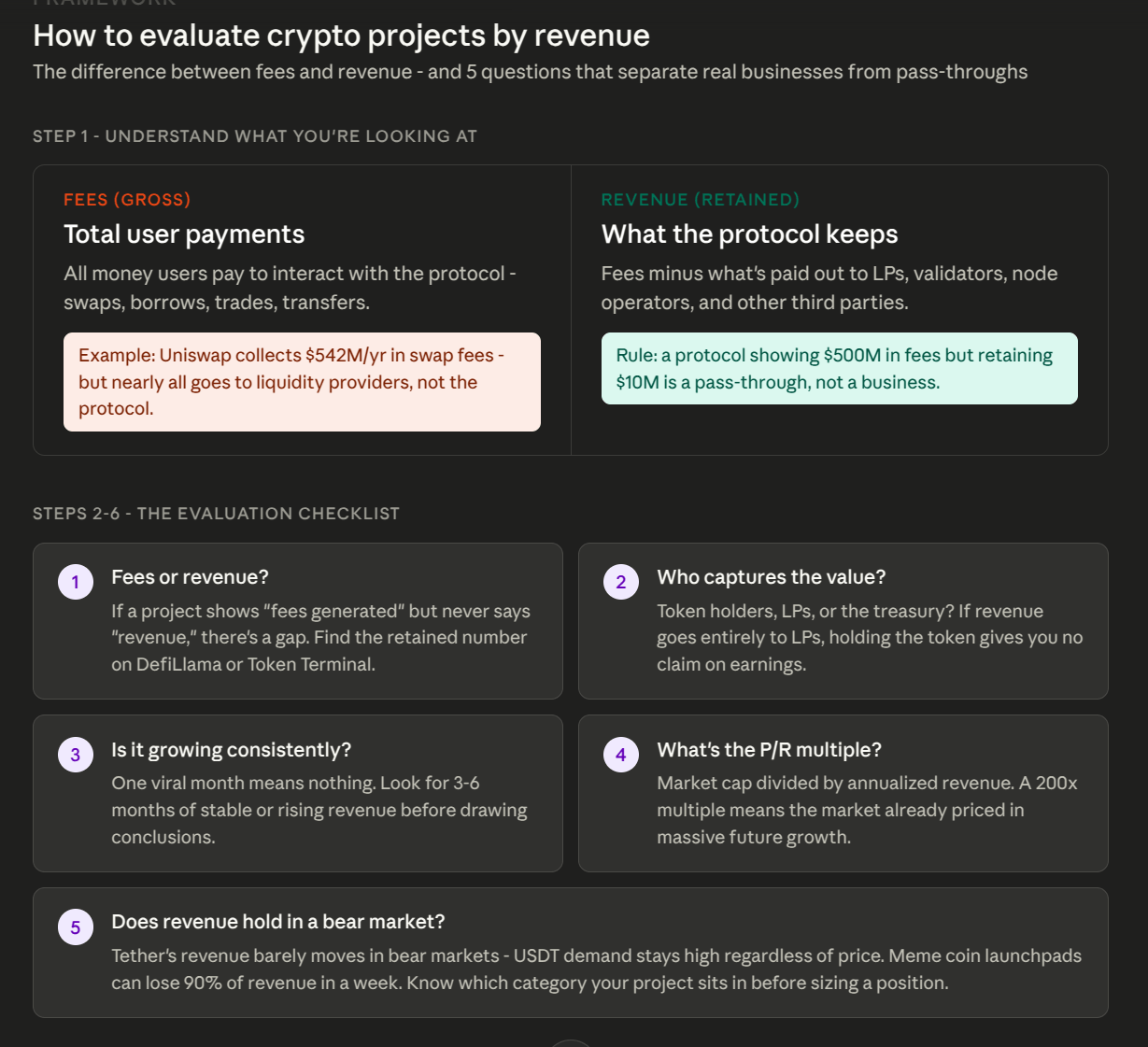

Fees = total money users pay to use a protocol.

Revenue = the portion of those fees the protocol itself keeps - after paying liquidity providers, validators, and other third parties.

A protocol can show $500 million in fees and only retain $10 million. That gap is the difference between a business and a pass-through. According to DefiLlama, which is the most reliable public source for this data, revenue is defined as total fees minus what gets distributed to supply-side participants (lenders, liquidity providers, node operators).

When someone says a DeFi protocol "earns" a number, always ask: fees or revenue? They are not the same thing.

Which Crypto Projects Make the Most Money Right Now?

Here are the top revenue-generating crypto protocols based on the most recent available data from Token Terminal and CoinGecko Research.

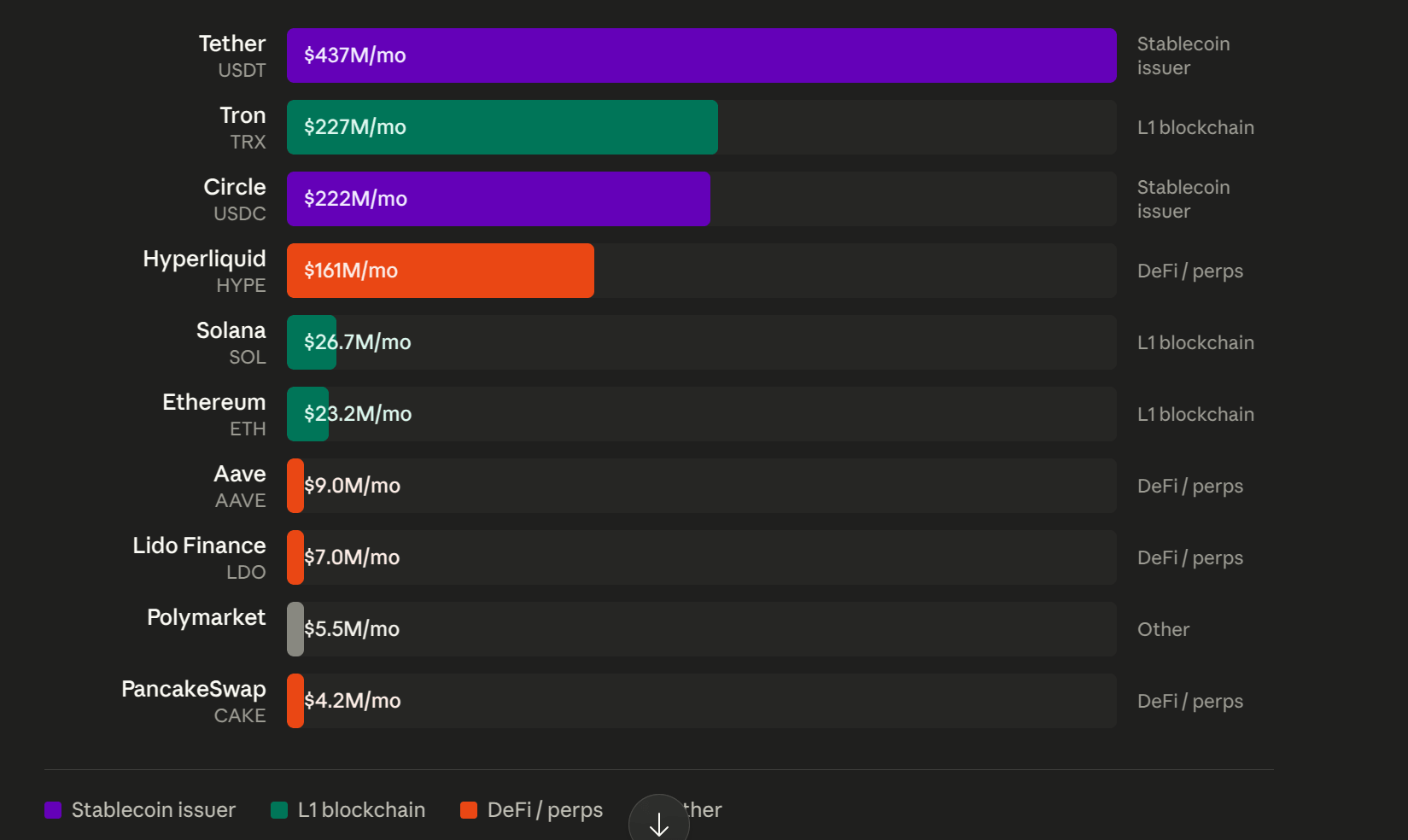

1. Tether (USDT) - ~$437M per month

Tether is not a blockchain. It is not a DeFi protocol. It is a company that issues the most widely used stablecoin in the world and parks the backing reserves in short-term US Treasuries and similar instruments.

The business model is straightforward: users deposit dollars, Tether issues USDT, and the company earns interest on the reserves. With roughly $185 billion worth of USDT in circulation, the interest income at current rates produces somewhere between $400-460 million per month depending on the period.

In 2025, Tether generated $5.2 billion in total revenue - 41.9% of all revenue across 168 tracked crypto protocols, according to CoinGecko Research. That is not a typo. One company took nearly half of all crypto protocol revenue for the year.

Revenue model: Reserve yield (interest on US Treasuries backing USDT)

Moat: Distribution - USDT is already embedded in every major exchange and payment rail globally

2. Tron (TRX) - ~$227M per month

Tron is the dominant blockchain for USDT transfers, particularly in Asian markets and for cross-border dollar settlements. Over 55% of global USDT transfers route through Tron because the fees are cheap and settlement is fast. That volume produces consistent transaction fee revenue regardless of what the broader market is doing.

In Q1 2026, Tron generated $67.33 million in fees and revenue in a single quarter, making it the revenue leader among L1 blockchains in that period, according to the Q1 2026 NFTPlazas industry report. As of April 2026, Tron is generating approximately $1.09 million in daily on-chain revenue - more than Ethereum, Solana, and BNB Chain combined on comparable days.

Revenue model: Transaction fees from stablecoin transfers

Moat: USDT routing inertia - once wallets and exchanges are integrated, they rarely switch

3. Circle (USDC) - ~$222M per month

Circle runs the same basic model as Tether: issue USDC, earn yield on the backing reserves. The difference is regulatory positioning. Circle is US-registered, MiCA-compliant in Europe, and has a compliance-first approach that has made it the preferred stablecoin for institutions and fintech partners.

USDC has a smaller float than USDT (roughly $60 billion vs $185 billion), so revenue is lower, but the reserve composition tends to be more conservative and fully audited. According to Token Terminal data, the top three protocols (Tether, Tron, Circle) alone account for over 82% of combined top-10 revenue.

Revenue model: Reserve yield on USDC backing

Moat: Institutional relationships and regulatory compliance

4. Hyperliquid (HYPE) - ~$161M in Q1 2026

Hyperliquid is the first DeFi protocol to genuinely threaten centralized derivatives exchanges on their own terms. It runs a fully on-chain order book for perpetual futures, with execution speed and liquidity that were previously only possible on centralized platforms.

In Q1 2026 alone, Hyperliquid generated over $180 million in fees and $161 million in retained revenue, making it the highest-revenue DeFi application in the quarter according to the NFTPlazas Q1 2026 report. The model routes 97% of platform fees into token buybacks, creating a direct connection between trading volume and token value.

Open interest in its HIP-3 markets hit $2.1 billion on March 31 - more than 100x growth from launch levels six months prior. That kind of traction in a bear market quarter says something real about the product.

Revenue model: Trading fees from perpetual futures contracts

Moat: On-chain order book performance that now matches CEX execution

5. Polymarket - $24M+ cumulative, with $1.71M single-day record

Prediction markets were niche two years ago. They are not niche anymore. Polymarket reached 606,000 monthly active users in January 2026 and holds 65.6% market share in on-chain prediction markets.

Its revenue crossed $24 million in cumulative fees, with a single-day record of $1.5 million on April 2, 2026, and a peak daily revenue of $1.71 million that ranked it fifth among all crypto protocols. Revenue comes from a small take rate on winning payouts.

Revenue model: Protocol take rate on resolved prediction markets

Growth driver: Real-money event markets move faster and more accurately than polls or news - this creates genuine utility that keeps users coming back

Which Blockchains Do Actually Make Money?

There is a difference between application-layer revenue (protocols like Tether, Hyperliquid) and network-layer revenue (the blockchain itself collecting transaction fees).

For February 2026, network revenue by blockchain ranked as follows, according to data from Solana Daily shared by Rand Group:

- Solana - $26.7 million

- Tron - $24.4 million

- Ethereum - $23.2 million

- BNB Chain - $9.3 million

- Base - $8.4 million

- Bitcoin - $5.5 million

Ethereum has historically dominated this ranking. The fact that Solana and Tron both matched or exceeded it in February 2026 reflects a real shift in where on-chain economic activity is happening - not just a one-time anomaly.

Tron's $24.4 million in network revenue is almost entirely driven by USDT transfer volume. Solana's lead came from 755% year-over-year growth in total payment volume, the highest of any chain or fintech platform tracked in the period.

Best DeFi Projects by Actual Revenue, Not Speculation

Speculation-driven metrics like TVL and token market cap can be inflated by a handful of whales. Revenue cannot. Here are the DeFi protocols with real, verified on-chain revenue streams in 2026.

Aave (AAVE)

Aave is the largest decentralized lending protocol, sitting at $10-12 billion in TVL across Ethereum, Polygon, Arbitrum, Base, and other chains. It earns the spread between borrowing and lending rates, plus liquidation fees when undercollateralized positions get closed out.

Revenue scales directly with market activity and borrowing demand. During periods of high leverage appetite, Aave's income rises meaningfully. DeFiLlama consistently ranks it among the top 10-15 revenue-generating protocols. The Aave V4 upgrade, currently in development, includes a GHO stablecoin expansion that could add a new revenue layer on top of the existing lending book.

Lido Finance (LDO)

Lido takes a 10% cut of all staking rewards generated by ETH it stakes on behalf of users. With over $10.2 billion in TVL as of mid-2026, that commission adds up to consistent monthly revenue even in flat markets.

The business model is simple: hold nothing, operate the staking coordination layer, collect fees on yield generated by others. Lido has crossed $750 million in cumulative protocol revenue. The risk is Ethereum staking yield compression if the validator set grows too large - but Lido's distribution dominance means it captures whatever yield is available.

Sky (formerly MakerDAO)

Sky, which rebranded from MakerDAO, earns stability fees charged on DAI borrowed against collateral. It also earns yield on its real-world asset portfolio, which includes US Treasuries and other instruments. CoinGecko identified Sky as one of the four stablecoin-adjacent protocols that dominated 2025 revenue, alongside Tether, Tron, and Circle.

PancakeSwap (CAKE)

PancakeSwap is the largest DEX on BNB Chain by volume. Revenue comes from a cut of swap fees on its AMM. The platform has been going through a rough period - revenue dropped 39.9% in recent months as BNB Chain activity has shifted toward newer protocols. PancakeSwap v3 concentrated liquidity and a gaming marketplace are the main growth bets, but the decline is real and worth monitoring.

On-Chain Revenue vs Market Cap: What the Ratio Tells You

This is one of the most useful filters I use when evaluating any crypto project. Take the protocol's annualized revenue and divide it into the token's market cap. You get a price-to-revenue multiple - the crypto equivalent of a P/S ratio.

Some benchmarks from current data:

- Tether: Annualized revenue ~$5.2B, but USDT itself is not a token with a float market cap - Tether Limited is a private company

- Hyperliquid: Annualized revenue running at ~$640M+ based on Q1 trajectory; HYPE market cap around $15B, giving a roughly 23x P/R multiple

- Aave: Monthly revenue in the $7-10M range; annualized ~$100M; market cap ~$3B = roughly 30x P/R

High multiples are not automatically bad - growth matters - but they tell you how much future growth is already priced in. A protocol with a 200x P/R multiple needs everything to go right. A protocol at 15-20x with growing revenue has room.

DefiLlama's advanced dashboard shows price-to-fees and price-to-revenue ratios directly. Token Terminal does the same. Both are free to use.

Centralized vs Decentralized Protocol Revenue: The Uncomfortable Truth

The data does not lie: centralized or semi-centralized structures dominate crypto revenue.

Tether, Circle, and to some extent Tron all depend on centralized control of reserve assets or network governance. Together they represent close to 75% of all tracked protocol revenue according to DL News analysis of 2025 data.

The reason is structural. Reserve-based models scale with assets under management and have near-zero marginal cost. A decentralized protocol like Uniswap has to compete on every trade and share most fees with liquidity providers. Tether just parks dollars in treasuries.

That said, the gap is narrowing from the application layer up. Hyperliquid, EdgeX, Lighter, and Axiom together generated around 7.5% of industry revenue in 2025, according to DL News State of DeFi 2025. If perpetuals keep growing at their current pace, they may genuinely rival stablecoin revenue by 2027.

Ethena (ENA) Revenue Growth 2026

Ethena runs a synthetic dollar protocol called USDe, which generates yield by combining staked ETH with short ETH perpetual positions. When funding rates are positive (traders pay to hold long positions), Ethena earns that funding as revenue.

This model works exceptionally well during bull markets when funding rates run high. Revenue growth was strong through 2025. The risk is a bear market where funding rates flip negative - in that scenario, Ethena has to cover funding payments rather than collect them, which drains the reserve. CoinGecko identified Ethena among the protocols generating significant revenue through its USDe token.

It is a smart construction, but it carries directional risk that pure reserve models do not.

How to Evaluate Crypto Projects by Revenue: A Practical Checklist

These are the exact questions I run through before I take any project seriously:

1. Fees vs revenue - which number are they showing you?

If a project's pitch deck shows "fees generated" but avoids the word "revenue," there is likely a large gap between the two. Find the revenue number on DefiLlama or Token Terminal.

2. Who captures the value - token holders, LPs, or the treasury?

Some protocols send all revenue to LPs and nothing to token holders. Owning the token in that case gives you no claim on earnings. Check the tokenomics documentation.

3. Is revenue growing month-over-month, or was there one big spike?

A single month of high revenue from a viral event means nothing. Look for 3-6 months of consistent growth or stability.

4. What is the price-to-revenue multiple?

If the market cap is 200x annualized revenue, the market is pricing in enormous growth. Calculate whether that growth is realistic based on the market size the protocol is competing in.

5. Can revenue hold in a down market?

Tether's revenue barely changes in bear markets because USDT demand stays high regardless of price. Meme coin launchpads can lose 90% of revenue in a week. Know which category your project sits in.

Crypto Fundamental Analysis Revenue Metrics: Where to Find Real Data

- DefiLlama (defillama.com/revenue) - Best for DeFi protocol revenue, updated daily. The advanced view includes treasury revenue, supply-side revenue, net earnings, and P/R ratios.

- Token Terminal (tokenterminal.com) - Best for structured financial statements on blockchain projects. Covers 302 protocols with standardized revenue accounting.

- CoinGecko Research - Publishes quarterly and annual revenue reports with sector breakdowns.

- The Block Data - Tracks top protocols by daily revenue with historical charts.

These four sources cross-reference each other well. When all four agree on a number, trust it. When they diverge, dig into the methodology difference before drawing conclusions.

Conclusion

The most profitable crypto projects by revenue in 2026 are not the ones with the most Twitter followers or the flashiest roadmaps. They are:

- Stablecoin issuers (Tether, Circle) with near-monopoly positions in dollar-denominated settlement

- Tron, which routes the majority of global USDT traffic and collects consistent fees for doing so

- Hyperliquid, which built a derivatives exchange good enough to take share from centralized platforms

- Aave and Lido, which have turned DeFi primitives into durable fee-generating businesses

Price and narrative move in cycles. Revenue moves with real usage. If you want to know which crypto projects are worth serious attention, start with the revenue rankings - and update them every month.